The introduction of Making Tax Digital for Income Tax (MTD for ITSA) represents the most significant reform to Self-Assessment in decades. For millions of sole traders and landlords, the way tax obligations are reported and managed will undergo a fundamental shift from an annual process to a quarterly digital system. Understanding these changes is essential for taxpayers and their advisers as the rollout approaches.

What is Making Tax Digital for Income Tax?

Making Tax Digital for Income Tax is HMRC's initiative to modernise the tax system by requiring taxpayers to keep digital records and submit updates throughout the year using compatible software. The reform builds on the existing MTD framework already in place for VAT-registered businesses.

From April 2026, self-employed individuals and landlords with qualifying income above £50,000 will be required to join MTD for ITSA. Those with an income between £30,000 and £50,000 will follow from April 2027, and from April 2028, those with an income between £20,000 and £30,000 will follow.

The thresholds apply to business or property income, not total taxable income.

The New Quarterly Submission Process Under MTD for ITSA

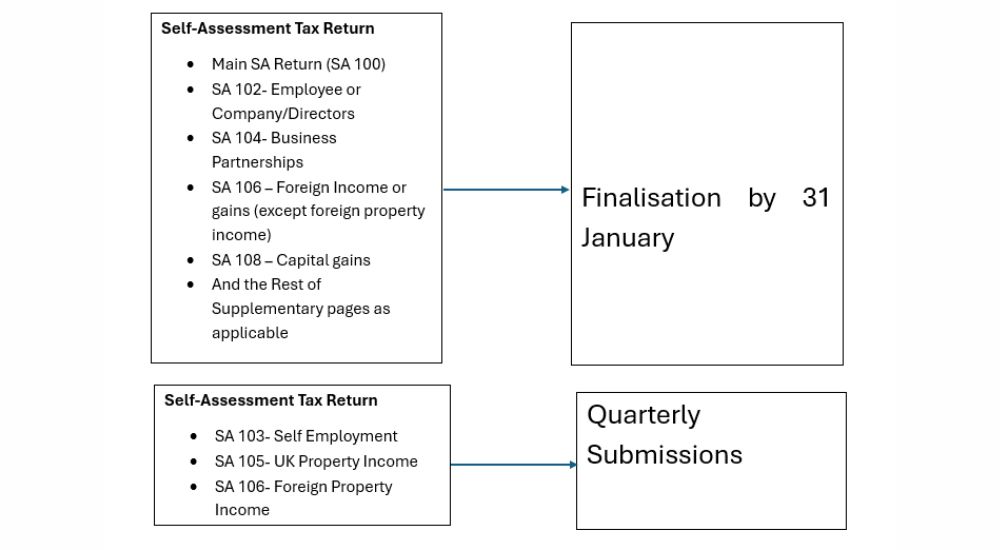

Under MTD for ITSA, taxpayers will move away from submitting a single annual tax return to providing quarterly updates on their business and property income throughout the year.

Quarterly Updates for Business and Property Income

Sole traders completing the SA103 self-employment pages and landlords completing the SA105 property pages will need to submit digital updates four times per year. These updates must be submitted using MTD-compatible software and will cover:

Business income and expenses for sole traders

Property rental income and allowable expenses for landlords

Each quarterly update must be submitted within one month of the end of the relevant quarter. For example, if your quarters align with the tax year, the first update covering 6 April to 5 July must be submitted by 5 August.

The quarterly submissions replace the annual completion of SA103 and SA105 pages. Instead of calculating your profit or loss once a year, you will be providing this information four times during the tax year.

What Happens to the Rest of the Self-Assessment Return?

Not all income sources are moving to quarterly reporting. The main Self-Assessment tax return and other supplementary pages will continue to operate on an annual basis, with a key difference in terminology and process.

Income that does not fall under MTD for ITSA quarterly reporting, such as employment income, dividend income, capital gains, foreign income and pension income, will be reported through what HMRC calls the "End of Period Overview" and "Final Declaration". This process effectively replaces the traditional Self-Assessment tax return, although the content remains similar.

The Final Declaration must be submitted by 31 January following the end of the tax year, maintaining the existing Self-Assessment deadline. This is when you finalise all your tax affairs for the year, including income sources not covered by quarterly updates.

Understanding the Finalisation Process

The finalisation stage combines your quarterly updates with other income sources to calculate your total tax liability for the year.

Consolidating Your Tax Position

Once you have submitted your four quarterly updates for business and property income, you will need to complete your Final Declaration. This involves:

Reviewing and confirming the information already submitted in quarterly updates

Adding details of any other income sources not covered by quarterly reporting

Claiming any additional reliefs or allowances

Making any necessary adjustments or corrections

The Final Declaration is when your complete tax position is established and any balancing payment or refund is calculated.

The 31 January Deadline Remains

Despite the shift to quarterly reporting for some income, the 31 January deadline remains the key date in the tax calendar. By this date, you must complete your Final Declaration and pay any outstanding tax due.

It is important to note that quarterly updates are not tax payments. They are simply information updates. Tax payments will continue to be made through payments on account and balancing payments, following the existing Self-Assessment payment schedule.

Key Practical Implications of MTD ITSA for Taxpayers

The move to MTD for ITSA brings several practical changes that taxpayers and advisers need to prepare for.

Digital Record Keeping Requirements

All taxpayers within MTD for ITSA must maintain digital records using MTD software that can connect to HMRC systems. Paper records or basic spreadsheets that cannot link to HMRC will no longer be acceptable.

The software must be capable of:

Recording income and expenses digitally

Calculating quarterly summaries

Submitting updates directly to HMRC through the API

Many accounting software providers already offer MTD-compatible solutions, and the market continues to develop as the implementation date approaches.

Increased Engagement Throughout the Year

Rather than focusing on taxes only once a year, taxpayers will need to engage with their tax affairs on a quarterly basis. This requires better organisation and more frequent interaction with your records and software.

For many, this will mean more regular contact with their accountant or tax adviser, particularly in the early stages of adoption. Establishing good routines for recording transactions and preparing quarterly updates will be essential.

Potential Benefits of Quarterly Reporting

While the change requires adjustment, quarterly reporting offers some advantages:

Earlier identification of errors or omissions

Better cash flow management through more regular review of financial position

Reduced year-end pressure when finalising tax affairs

More accurate tax calculations throughout the year

HMRC's stated aim is to reduce errors and make tax administration simpler in the long term, although the transition period will require effort and adaptation.

What Stays the Same After MTD for ITSA?

Despite the significant changes, some aspects of Self-Assessment remain unchanged:

The tax year continues to run from 6 April to 5 April

Tax payment dates remain the same (payments on account due 31 January and 31 July, with balancing payment due 31 January)

The 31 January deadline for finalising your tax affairs continues

The underlying tax rules and calculations are not changing

Penalties for late submission and late payment continue under the existing framework (although penalty rules for quarterly updates are still being finalised)

Who Must Comply with MTD for ITSA and What Are the Key Dates?

From April 2026: Self-employed individuals and landlords with business or property income over £50,000 per year

From April 2027: Self-employed individuals and landlords with business or property income between £30,000 and £50,000 per year

From April 2028: Self-employed individuals and landlords with business or property income between £20,000 and £30,000 per year

Partnerships will follow in later phases, with details still to be confirmed by HMRC.

Taxpayers whose business or property income falls below £30,000 will not be mandated to join MTD for ITSA, although they may choose to opt in voluntarily.

Preparing for MTD ITSA Changes

With the implementation date approaching, now is the time to prepare:

Check if you will be affected by reviewing your business or property income against the thresholds

Consider your software options and ensure you have MTD-compatible accounting software in place well before your start date

Review your record-keeping processes to ensure they are suitable for digital reporting

Speak to your accountant or tax adviser about how MTD for ITSA will affect your specific circumstances

Familiarise yourself with the quarterly submission requirements and plan your workflow accordingly

Conclusion

Making Tax Digital for Income Tax represents a fundamental shift from annual to quarterly reporting for business and property income. While the SA103 and SA105 elements of Self-Assessment move to quarterly digital updates, the main tax return and other supplementary pages continue as an annual finalisation process, due by 31 January.

The change requires preparation, investment in software and adjustment to new ways of working. However, with proper planning and support, taxpayers can navigate the transition successfully and potentially benefit from more regular engagement with their tax affairs.

As the implementation dates draw closer, staying informed and taking early action will be key to a smooth transition to the new digital tax system.