.jpg)

If you're an IT consultant or contractor operating as a sole trader, Making Tax Digital for Income Tax (MTD For ITSA) is about to fundamentally change how you report your income to HMRC. From April 2026, thousands of IT professionals will be required to switch from traditional Self-Assessment to quarterly digital reporting.

This comprehensive guide explains exactly how Making Tax Digital for IT consultants works, when you need to comply, what software you'll need, and the penalties you'll face for non-compliance.

What Is Making Tax Digital for Income Tax?

Making Tax Digital for Income Tax is HMRC's digital tax initiative requiring sole traders and landlords to keep digital records, submit quarterly updates of their income and expenses through compatible software and submit a final tax return to HMRC.

For IT consultants working as sole traders, this means:

Digital record-keeping using MTD-compatible software

Quarterly updates to HMRC (not quarterly payments - those rules haven't changed)

Annual tax return submission through your MTD software

New penalty regime with points-based late submission penalties

Important: MTD for Income Tax is separate from MTD for VAT. If you're already registered for MTD for VAT, you'll still need to comply with MTD for Income Tax separately.

Is Making Tax Digital Mandatory for IT Consultants in the UK?

Falling under MTD for IT consultants depends on your qualifying income - your total gross income from self-employment and property before expenses.

The Income Thresholds

You must use MTD for Income Tax for IT consultants if your qualifying income exceeds:

Tax Year | Income Threshold | MTD Start Date |

|---|---|---|

2024/25 | Over £50,000 | 6 April 2026 |

2025/26 | Over £30,000 | 6 April 2027 |

2026/27 | Over £20,000 | 6 April 2028 |

What Is Qualifying Income Under Making Tax Digital for IT Consultants?

Your qualifying income as MTD IT consultants includes:

All income from your IT consulting business (before expenses)

Any UK or foreign property rental income

Example: You're an IT consultant earning £45,000 from contracts, and you also rent out a property generating £8,000. Your total qualifying income is £53,000, meaning you'll need to use MTD from April 2026.

Calculate your Income for Qualifing MTD: Making Tax Digital Calculator

What Doesn't Count Toward Your Qualifying Income ?

Employment income (PAYE)

Partnership income or dividends (including from your own limited company)

State or private pensions

Savings interest or investment income

Key Point:

Many IT contractors operate through limited companies. If this is you, MTD for Income Tax doesn't apply to your company income - only to any separate sole trader consultancy work or property income you receive personally.

HMRC Reporting Obligations Under Making Tax Digital for IT Consultants

Quarterly Reporting Requirements

Under MTD for Income Tax, IT professionals must submit quarterly updates to HMRC - but these are not quarterly tax returns in the traditional sense. Here's what you need to know:

What quarterly updates contain:

Each HMRC quarterly update is a summary of your income and expenses for that quarter. You're reporting your business transactions - turnover, allowable expenses, and any other relevant business information. These updates give HMRC a real-time view of your trading activity throughout the year.

Standard Quarterly deadlines:

MTD for Income Tax has fixed quarterly deadlines:

_ - visual selection.png)

Calendar Quarter Option for IT Consultants

While most IT consultants can use the standard quarterly update periods aligned with the tax year, MTD for Income Tax offers an alternative: calendar quarter reporting.

_ - visual selection.png)

Whatever reporting quarter you choose, the submission deadline remains same for both options.

Important Considerations Before Choosing Calendar Quarters

You must decide before your first update: You need to choose your quarterly reporting option when you sign up for MTD for IT consultants. Once you've submitted your first quarterly update using either method, you generally cannot switch mid-year. This decision affects your entire MTD reporting structure.

Not all software supports calendar quarters: While HMRC allows calendar quarter reporting, not all MTD-compatible software products fully support this option. Before choosing calendar quarters, confirm your preferred software can handle calendar quarter submissions and reporting. Some bridging software products may have limitations.

What you're NOT doing: Quarterly updates are not tax calculations and don't determine what you owe. They're informational submissions that help HMRC track your business activity. You're not paying tax quarterly.

Updates can be revised: If you discover an error in a previous quarterly update, you can correct it in subsequent updates or during your final tax return submission.

Final Tax Return Submission Requirements

Despite submitting quarterly updates throughout the year, you still need to submit a final tax return - but the process changes significantly under Making Tax Digital for IT Consultants:

The crystallisation process: Your final tax return is technically called "final declaration" or "crystallisation" under MTD. This is where you confirm all your income and expenses for the year, make any final adjustments, and claim allowances and reliefs. It's submitted through your MTD software by 31 January following the end of the tax year.

What's different from quarterly updates:

While quarterly updates only cover self-employment and property income, your final return must include ALL income sources reported through Self-Assessment. This includes:

Self-employment income (already reported quarterly)

Property income (already reported quarterly)

Employment income (PAYE) if not fully taxed at source

Dividends and partnership income

Savings and investment income

Capital gains

Foreign income

Any other taxable income

Tax calculation and payment: Unlike quarterly updates, your final return under Making Tax Digital for IT Consultants triggers the actual tax calculation. HMRC will calculate what you owe based on all your income, apply any tax already paid through PAYE or payments on account, and determine if you have a balancing payment to make or are due a refund. This calculation must be completed and any balance paid by 31 January.

Key difference for IT consultants: If you have income from a limited company (dividends or salary), this must be included in your final return but NOT in your quarterly updates. Only report sole trader consultancy income in quarterly updates. All other income sources are reported once annually in the final submission.

Critical Deadlines Under Making Tax Digital for IT Consultants

Making Tax Digital for IT Consultants timeline is crucial for compliance. Here are the key MTD dates and deadlines you need to know:

Critical Note: Even if you receive a letter from HMRC confirming you need to use MTD, it's still your responsibility to check your eligibility and ensure you're signed up in time.

Check Your Making Tax Digital Eligibility With Our: MTD Checker

New Penalty System for MTD for IT Consultants

MTD for Income Tax for IT consultants introduces a completely new penalty regime that's significantly different from current Self-Assessment penalties.

Late Submission Penalties: Points-Based System

Instead of immediate financial penalties, MTD for ITSA uses a points system:

Annual tax return filing: You receive 1 point for each late submission. At 2 points, you're charged £200. Each subsequent late submission incurs another £200 penalty.

Quarterly filing: You receive 1 point for each late quarterly update. At 4 points, you're charged £200. Each subsequent late submission incurs another £200 penalty.

Good News: If you consistently submit all required filings on time for a continuous period, your penalty points will reset to zero. The reset period depends on your filing frequency:

Annual filers: Points reset after 24 months of on-time submissions.

Quarterly filers: Points reset after 12 months of on-time submissions.

Important conditions:

Every submission during this period must be received on time.

Any previous outstanding submissions must be completed before the reset can occur.

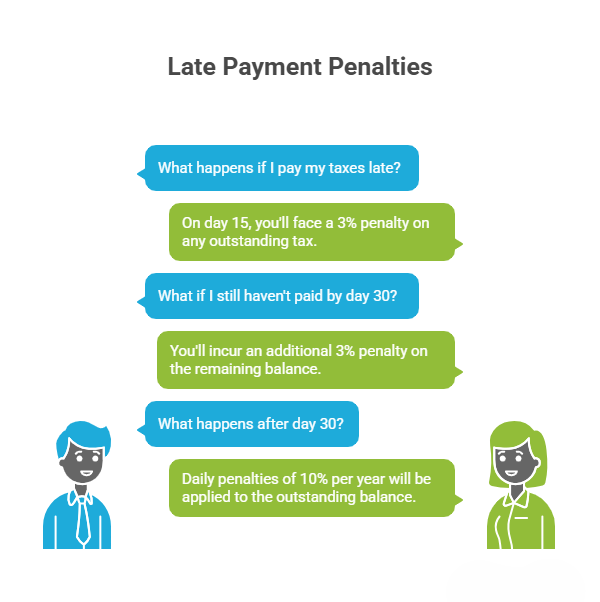

Late Payment Penalties: Much Harsher Than Before

The late payment regime is where MTD for ITSA gets seriously expensive:

Major Change: Current Self-Assessment gives you 30 days before any penalty. MTD for ITSA reduces this to just 15 days, and penalties compound rapidly. However, having a Time to Pay arrangement in place by the deadline prevents these penalties.

First-Year Soft Landing: Penalty Relief for 2026/27

The government confirmed that quarterly update penalties will be suspended during the first year of MTD implementation. This means if you're mandated to start using MTD for ITSA from April 2026 (because your 2024/25 qualifying income exceeded £50,000), you won't face penalty points for late quarterly updates during the entire 2026/27 tax year.

What this soft-landing covers for IT consultants under MTD:

No penalty points for late quarterly updates during 2026/27

Gives you breathing room to adjust to the new digital reporting system

Allows software providers time to onboard users efficiently

What the soft landing does NOT cover:

Late payment penalties - These still apply in full from day one. If you pay your tax late, you'll face the standard 3% penalties at 15 days, 3% at 30 days, and 10% per year thereafter

Annual tax return penalties - Your final declaration for 2026/27 (due 31 January 2028) is subject to normal late filing penalties under new penalty system.

Future years - The suspension only applies to 2026/27. From April 2027 onwards, quarterly update penalties apply normally

Later joiners - If you join MTD from April 2027 or later (income thresholds £30,000+), the penalty suspension doesn't apply to you

Important Note: While quarterly update penalties are suspended, you're still legally required to submit quarterly updates, maintain digital records, and file your annual final declaration. The suspension removes the financial penalty for mistakes, but compliance remains mandatory.

Other Penalties That Still Apply for IT consultants under MTD

Record-keeping failures: Up to £3,000 for failing to maintain digital records or digital links

Inaccuracy penalties: Apply to annual returns (but not quarterly updates)

Key Takeaways

Check your qualifying income now - Calculate your gross self-employment and property income to determine when you need to start using MTD

MTD starts April 2026 for £50k+ earners - If your 2024/25 qualifying income exceeds £50,000, you must use MTD from 6 April 2026

Quarterly updates are mandatory - You'll submit updates every three months (deadlines are fixed dates, not quarterly)

Penalties are new - Late payment penalties begin at just 15 days, and the points system means missed deadlines accumulate

Choose MTD-compatible software early - You need MTD software that handles digital records, quarterly updates, and annual returns

Your accountant needs software too - If you use an accountant or tax agent, they'll need compatible software to work on your behalf

Limited company income doesn't count - MTD only applies to sole trader and property income, not dividends or salary from your limited company

Sign up before your mandatory date - You can volunteer early to test the system, but must be signed up before your obligation begins

Worried About MTD Compliance for IT Consultants?

Choose the Right MTD Software for IT Consultants

Selecting the right MTD software for IT Consultants is one of your most important decisions. Your software must be able to:

Create and store digital records of income and expenses

Send quarterly updates to HMRC

Submit your annual tax return by 31 January

Report all income sources (not just self-employment)

Types of MTD Software for IT Consultants

Software that creates digital records -

Most comprehensive option for IT consultants. These products typically offer:

Bank feed integration to automatically import transactions

Receipt scanning via mobile apps

Expense categorisation

Mileage tracking

Invoice generation

Direct submission to HMRC

Connects to your existing spreadsheets or accounting tools. Useful if:

You have a record-keeping system you want to keep using

You use industry-specific software that isn't MTD-compatible

You prefer detailed control over your records

Essential Features of MTD Software for IT Consultants

When evaluating MTD software, prioritise these features:

Multiple income source support - Many IT consultants have varied income streams (contracts, advisory work, training, property)

Agent access - If you use an accountant, ensure they can access your records

Expense management - Robust categorisation for home office costs, equipment, subscriptions, travel

Reporting capabilities - Real-time visibility of your tax position

Special Considerations about MTD for IT Consultants

Working Through Both Limited Company and Sole Trader

Many IT professionals have hybrid arrangements - a limited company for main contracts and sole trader income for smaller advisory work. MTD for ITSA only applies to your sole trader income.

Foreign Income and Non-UK Residence Under MTD for IT Consultants

IT consultants working internationally need to understand how tax residence affects MTD:

UK tax residents: All self-employment and property income (UK and foreign) counts toward qualifying income

Non-UK residents: Only UK property and UK self-employment income declared on your UK return counts

If Your Income Fluctuates

IT consulting income can be volatile. Key points:

HMRC assesses your previous year's gross income to determine if you're in scope

Even if you stop trading, ceased income still counts in the calculation that determines your mandate for the upcoming year

If you're mandated but your income drops below the threshold for 3 consecutive years, you can opt out

Making Tax Digital Exemptions for IT Consultants

You may be exempt if it's not reasonable for you to use digital record-keeping software. This is rarely applicable to IT professionals given their technical capabilities, but exemptions exist for:

Those unable to use computers due to age, disability, or location

Religious objections to using computers

Other exceptional circumstances

Ready to Tackle MTD with Confidence?

Rentalbux, HMRC Recognised MTD software provides comprehensive MTD support designed specifically for UK IT Consultants. Our affordable, user-friendly platform handles all your MTD compliance requirements automatically.

Features Highlights:

Designed by Accountants Who Work with IT Consultants

IT Consultant-Specific Chart of Accounts

Simple Enough for Non-Accountants

Digital Records

Quarterly Update Filing

Final Declaration

The Bottom Line

Making Tax Digital for Income Tax represents the biggest change to self-employment and property tax reporting in decades. For IT consultants operating as sole traders, compliance isn't optional - it's mandatory if your qualifying income exceeds the thresholds.

The good news? With the right preparation and software, MTD can actually simplify your tax administration. Quarterly updates help you stay on top of your tax position throughout the year, rather than facing a stressful scramble every January. Digital record-keeping makes expense tracking easier, and modern software often provides better insights into your business finances.

The key is to start preparing now. Don't wait until a few weeks before your mandatory start date. Research your options, choose appropriate software, and if possible, sign up voluntarily to test your setup. The penalties for non-compliance are significant, but with proper planning, MTD for IT consultants can become a routine part of your business operations.