.jpg)

The digital transformation of UK tax reporting is here, and architects need to prepare. Making Tax Digital for Income Tax (MTD For ITSA) represents the most significant change to self-assessment reporting in decades. Whether you run an architectural practice as a sole trader or earn property income from development projects, understanding how MTD affects your business is crucial for staying compliant.

This comprehensive guide breaks down everything architects need to know about MTD, from qualification thresholds to software requirements, ensuring you're ready when mandatory reporting begins in April 2026.

Key Takeaways: MTD for Architects

✓ Architects with qualifying income over £50,000 must use MTD from April 2026

✓ Qualifying income includes architectural practice turnover and property income (before expenses)

✓ HMRC-recognised software is mandatory—start researching options now

✓ Quarterly updates are required four times per year, plus an annual return

✓ First-year penalty relief applies to quarterly updates in 2026-27 only

✓ Digital record-keeping must begin when you join MTD

✓ Your accountant can manage MTD on your behalf if properly authorised

What is Making Tax Digital for Architects?

Making Tax Digital for Income Tax is HMRC's initiative to modernise tax reporting through digital record-keeping, quarterly submissions and final tax return submission. For architects operating as sole traders, this means transitioning from annual self-assessment returns to a system of regular digital updates throughout the tax year.

The system requires compatible software to:

Maintain digital records of income and expenses

Submit quarterly updates to HMRC

Complete your annual tax return digitally by 31 January

Do Architects Need to Use MTD for Income Tax?

As an architect, you'll need to use MTD for Income Tax if all of the following apply:

You're registered for Self-Assessment as a sole trader or landlord

You receive income from self-employment or property (or both)

Your qualifying income exceeds the relevant threshold

Understanding Qualifying Income for Architects

Your "qualifying income" is your gross income (turnover before expenses) from:

Self-employment as an architect

UK property rental income

Foreign property rental income (if UK tax resident)

Important: Qualifying income does NOT include:

Partnership income

Dividends from your limited company

PAYE employment income

Pension income

MTD Thresholds and Timeline for Architects

The rollout of MTD for Income Tax follows a phased approach based on qualifying income thresholds:

.png)

Check Your Status

If your architectural practice had qualifying income over £50,000 in the 2024-25 tax year, HMRC should write to you confirming you need to start using MTD by 6 April 2026. However, it's your responsibility to verify your status regardless of whether you receive a letter.

MTD Exemptions Relevant to Architects

Several exemptions may apply to architects, though most won't qualify:

Digital Exclusion

Digital exclusion is one of the few exemptions that architects might genuinely qualify for, though HMRC sets a high bar for approval. Being digitally excluded from Making Tax Digital for Income Tax means it's not reasonable for you to use MTD compatible software to keep digital records or submit them to HMRC.

Valid reasons for digital exclusion (case-by-case assessment):

Your age prevents you from using computers, tablets or smartphones

You have a disability that stops you from using digital devices (e.g., severe visual impairment, motor disabilities)

You have a health condition that makes digital record-keeping unreasonable (e.g., cognitive impairments, degenerative conditions)

You're a practising member of a religious society whose beliefs are incompatible with digital communications, and you don't use computers, tablets or smartphones for business or personal use

You cannot get internet access at your home or business premises due to your location

You cannot get internet access at any suitable alternative location

MTD Software for Architects

Choosing the right MTD software for architects is crucial. Your software must enable you to:

Create and store digital records of architectural income and project expenses

Send quarterly updates to HMRC four times per year

Submit your annual tax return by 31 January following the tax year

Types of MTD Software for Architects

Record-creating software provides architects with a complete, all-in-one solution for managing both their practice finances and Making Tax Digital compliance. It typically connects directly to your business bank account to automatically import transactions, supports receipt and invoice scanning, and allows manual entry for cash expenses. This type of software handles all MTD requirements in one place, making it ideal for architects who want a streamlined system without relying on spreadsheets or multiple tools.

Bridging software, on the other hand, is designed for architects who already use spreadsheets or existing accounting systems and prefer minimal change to their current processes. It connects your existing records to HMRC, allowing you to continue working in familiar formats while still submitting quarterly updates and annual returns digitally. This option suits architects with established record-keeping systems who want to remain compliant without switching to new accounting software.

Essential Features of MTD Software for Architects

When selecting MTD software, ensure it supports:

Self-employment income tracking for architectural services

Property income reporting if you have rental properties

Expense categorisation relevant to architectural practices

Project-based accounting for tracking individual commissions

Multi-currency support for international projects (if applicable)

Agent access if you work with an accountant or tax adviser

Standard or calendar update periods matching your accounting approach

Get MTD-Ready with RentalBux

Don't let Making Tax Digital catch you unprepared. RentalBux offers HMRC-recognised MTD software designed specifically for landlords and sole traders like architects who combine professional practice with property income.

✓ Property management features

✓ Digital record-keeping

✓ Annual return completion

✓ User-friendly interface for tax compliance

Quarterly Update Requirements for Architects

Once you join MTD, you'll submit quarterly updates summarising your:

Income from architectural services

Business expenses

Property income (if applicable)

Standard Quarter Deadlines

Updates are due within one month of the end of each quarter. For the standard tax year:

Standard Quarter Deadlines

You can also choose calendar quarters if that suits your practice better. Once selected, your updates must continue to follow the same quarterly pattern consistently.

Quarters | Submission Deadlines |

|---|---|

1 April – 30 June | 7 August |

1 July – 30 September | 7 November |

1 October– 31 December | 7 February |

1 January – 31 March | 7 May |

Cumulative Record-Keeping Under MTD

Under Making Tax Digital, your records and quarterly updates are cumulative. This means each quarterly submission includes year-to-date totals, not just the figures for that individual quarter.

For example, your Q2 update will show income and expenses from 6 April up to 5 October (or from 1 April to 30 September if using calendar quarters), not only the activity in that three-month period. The same approach continues for Q3 and Q4.

Cumulative reporting allows you to:

Correct errors from earlier quarters in later updates

Maintain a running view of your tax position throughout the year

Avoid resubmitting previous quarters separately

First-Year Penalty Relief (2026-27 Only)

Good news: The Autumn Budget 2025 confirmed that penalty points for late quarterly updates will be suspended during the 2026-27 tax year for those joining in April 2026.

This "soft landing" applies only to:

Quarterly update penalties

First-year MTD users (April 2026 joiners)

It does NOT cover:

Late payment penalties

Late annual return submission

Those joining from April 2027 onwards

You must still submit quarterly updates—you just won't receive penalty points for late submissions during your first year.

Annual Tax Return Under MTD

Despite submitting quarterly updates under Making Tax Digital, you will still need to complete an annual tax return, known as the final declaration, by 31 January following the end of the tax year. This final submission confirms your overall tax position for the year, allows you to make any necessary adjustments or corrections to earlier updates, and includes income that is not reported quarterly, such as employment earnings, pensions, dividends, or partnership income. It also calculates your final tax liability, ensuring everything is accurately reported to HMRC.

New Penalty System for Architects Under MTD

MTD introduces a points-based penalty system replacing the current fixed penalties.

Late Submission Penalties

Annual returns:

First late return = 1 penalty point

Second late return = another point (total 2 points)

At 2 points = £200 penalty

Each subsequent late return = another £200 penalty

Points reset to zero after 24 months of on-time submissions (once all outstanding returns are filed).

Quarterly updates (from 2027-28 onwards):

Each late update = 1 penalty point

Second late return = another point (total 2 points)

At 4 points = £200 penalty

Each subsequent late return = another £200 penalty

Points reset after 12 months of on-time submissions

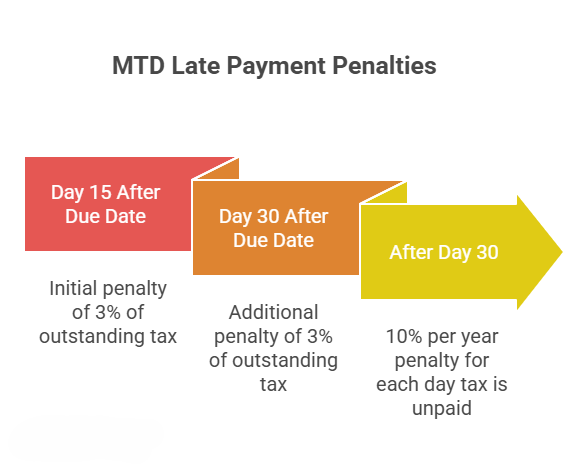

Late Payment Penalties

Late payment penalties are significantly harsher under MTD:

First-year relief:

All taxpayers get an additional 15 days (30 days total) before the first late payment penalty applies in their first year under the new system.

Critical: These penalties apply ON TOP of interest charges. Having a Time to Pay arrangement in place before the penalty date avoids these charges.

Conclusion

Making Tax Digital for Income Tax marks a major shift in how architects manage their tax obligations, but with the right preparation it doesn’t have to be disruptive. Understanding whether you’re in scope, keeping accurate digital records, and choosing HMRC-compatible software will put you in control well before the April 2026 deadline. Early action also gives you time to adjust your processes and avoid unnecessary penalties.

By preparing now, architects can turn MTD into an opportunity rather than a burden—gaining clearer financial visibility, smoother collaboration with accountants, and peace of mind around compliance. The key is to start early, choose the right tools, and approach the transition with confidence rather than urgency.

Take Action Now

Making Tax Digital for Income Tax becomes mandatory in just months. As an architect, here's your action plan:

Calculate your qualifying income for 2024-25 today

Research MTD software options suited to architectural practices

Consult your accountant about MTD preparation

Sign up before the deadline to avoid last-minute stress

Consider RentalBux if you have both practice income and rental properties

The transition to digital tax reporting is inevitable—early preparation ensures you're compliant, confident, and ready for the future of UK tax administration.

FAQ Section