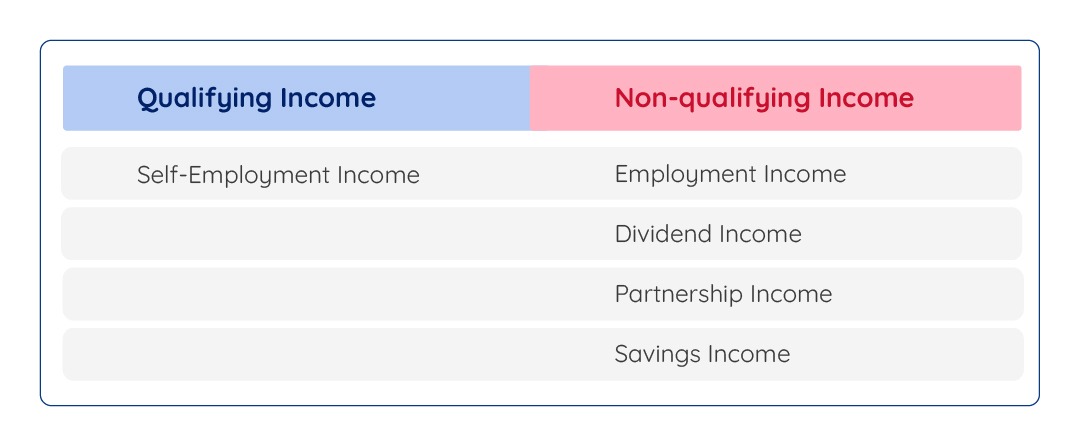

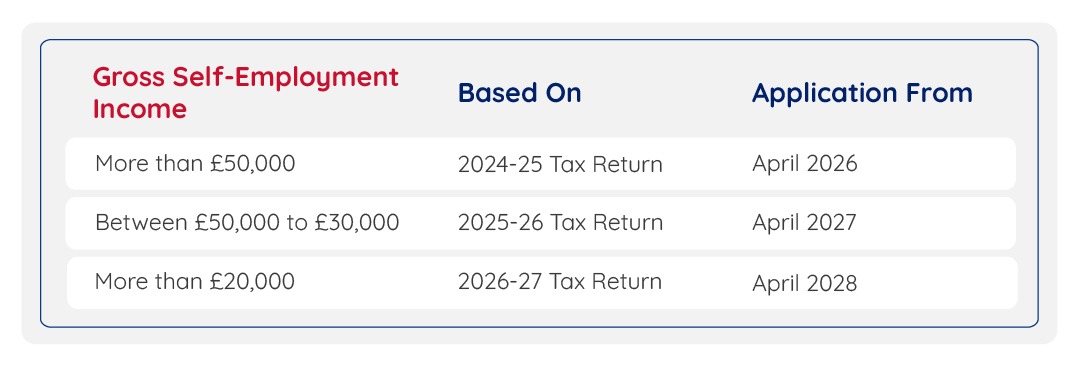

Record all business income, including sales, fees, takings, and other income, along with allowable expenses such as stock, travel, and office costs. If your turnover from self-employment is below the £90,000 VAT threshold, you can choose to submit simplified “three-line accounts” and categorise each item as income, expense, or net profit.

If you run multiple businesses, keep separate records for each. Store or scan all invoices and receipts, and if you use spreadsheets, maintain digital links using bridging software.